Financial technology: Products have benefits and risks for underserved consumers, and regulatory clarity is needed

What the GAO found

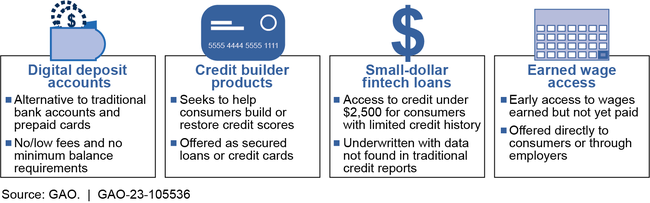

Fintech refers to the use of technology and innovation to offer financial products and services (see figure for selected products). Fintech products can offer benefits to underserved consumers, such as those without bank accounts or credit scores, but can also pose risks. For example, digital deposit accounts advertise low or no fees and no minimum balance requirements. However, consumers may be unaware that their money is not held by the fintech company itself, and may be confused about how to get their money back if the company goes out of business. Earned wage access purports to give consumers access to money that has been earned but not yet paid, potentially helping lower-income consumers meet financial obligations. But the cost of the product may not be transparent and there may be a risk of unexpected overdraft fees.

Overview of selected Fintech products

Some underserved consumers may face barriers in accessing fintech products – for example, they may lack internet access or prefer individualized or personal assistance from traditional banks. Data on the extent to which fintech products serve disadvantaged consumers is limited. However, one company that offers digital deposit accounts told the GAO that nearly half of its account holders are underbanked (ie, have bank accounts but use alternative financial services like payday loans, which can be costly) and 15 percent were previously unbanked. Data GAO received from four businesses with earned income access indicates that these products were used primarily by consumers earning less than $50,000 annually.

Regulators have taken some steps to address risks posed by select fintech products, but regulatory uncertainty exists for certain earned income access products. State and federal regulators have sought to better understand fintech products through measures such as information sharing agreements with companies. Federal financial regulators are changing their investigation processes to better monitor banks’ partnerships with fintech companies. The regulators have also issued guidance relating to selected fintech products. For example, the Consumer Financial Protection Bureau (CFPB) issued an advisory statement in November 2020 clarifying that earned income access products with specific features are not considered an extension of credit under the Truth in Lending Act. However, despite this guidance, some have expressed continued uncertainty about how the law applies to products that do not fall under the advisory opinion. Additional clarification may help companies offering these products understand whether the Act and its disclosure requirements apply.

Why GAO did this study

Millions of consumers face barriers to getting accounts and accessing credit through traditional banks and credit unions. In recent years, fintech has emerged as a potential way to help some underserved consumers access financial services. However, it is unclear how many underserved consumers use these products, what risks they may pose, and the extent to which existing financial services laws address these risks.

The Dodd-Frank Wall Street Reform and Consumer Protection Act includes a provision requiring the GAO to report annually on financial services regulation. This report examines (1) the benefits, risks, and limitations of selected fintech products for underserved consumers, and what is known about the extent to which underserved consumers have used them, and (2) federal and state regulators’ steps to evaluate selected fintech products . GAO reviewed studies by federal agencies, academics, and industry groups; analyzed data from selected fintech companies; and interviewed federal and state financial regulators, consumer groups, trade associations, and academics.