Important trends and growth opportunities in Kazakhstan’s Fintech highlighted in the report

ASTANA — A combination of a favorable business environment, robust banking infrastructure, supportive government policies and fintech regulations, along with a tech-savvy population, make Kazakhstan an attractive destination for foreign fintech investors and companies seeking growth opportunities, according to the report issued. April 13 by RISE Research, Kazakhstan’s MOST holding, and the international consulting company Fintech Consult.

Image credit: Forbes.com.

Among key trends identified of the report are the rise of digital payments and e-commerce, ecosystems, super-apps, digitization of small and medium-sized enterprises (SMEs), democratization of capital markets and an increase in fintech companies.

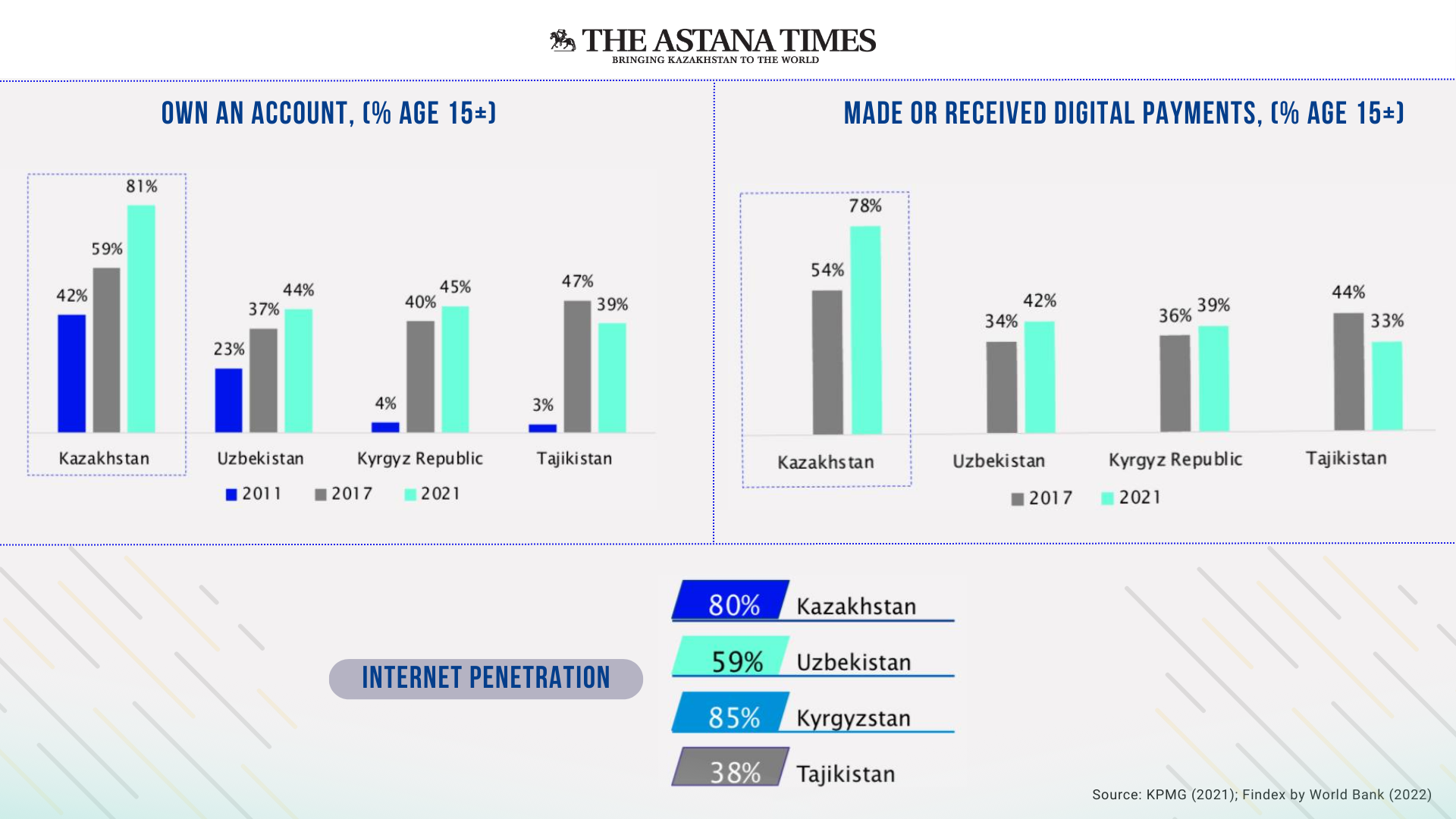

Kazakhstan’s leading position in improving financial inclusion and strong account and internet access are important drivers of digital payment use and prerequisites for favorable fintech development.

The country ranks first in the number of people who have a bank account, with 81 percent, followed by Kyrgyzstan and Uzbekistan, which have 45 percent and 44 percent respectively. Comparing the use of digital payments in Central Asia, Kazakhstan has a striking lead with 78 percent in 2021 compared to Uzbekistan with 42 percent and 39 percent in Kyrgyzstan.

The increase in digital payments and e-commerce

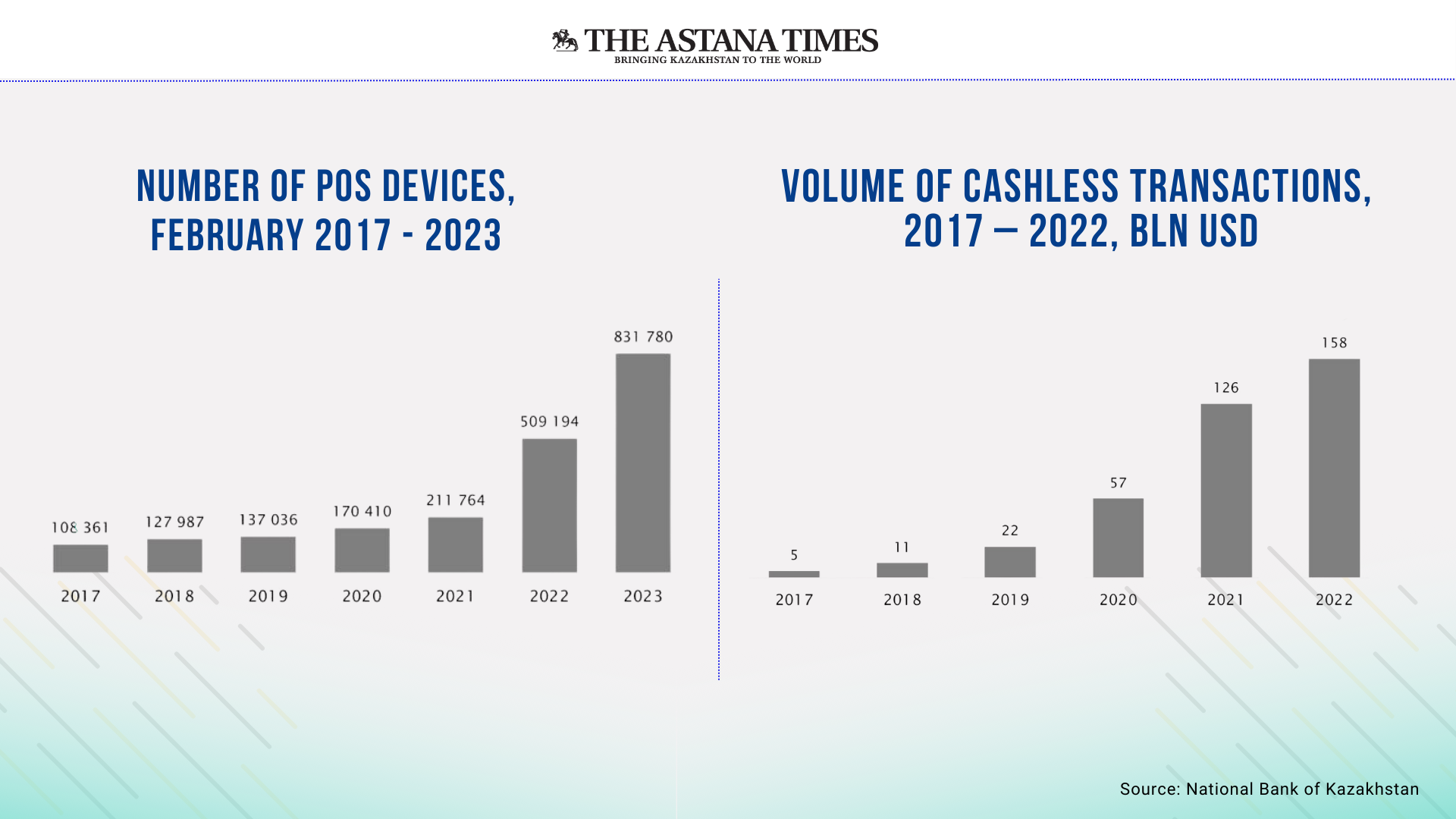

One of the main trends in the Kazakh fintech market is the rapid growth of digital payments and e-commerce. The volume of cashless transactions experienced staggering growth from $5 billion in 2017 to $158 billion in 2022. Key technologies changing the payment landscape include biometrics, advanced data analytics, instant transfers, digital customer consent management, open banking and central bank digital currencies (CBDC).

The popularity of new forms of payment, such as QR codes, among customers and merchants has led to an increase in cashless transactions. It is a convenient and affordable way to transact. The report says that point-of-sale (POS) devices, which enable retailers to manage inventory and process sales, grew from 108,361 devices nationwide in February 2017 to 831,780 in February 2023.

The rise of the ecosystem and adoption of super apps, which enable banks to offer customers a variety of services through a single application, is another trend that is changing daily life to a great extent. According to the report, 86 percent of the population actively use mobile banking services. These services combine financial and non-banking services, including online payment, mobile banking, e-commerce, investment and insurance.

According to the report, the competition among banks to offer more services integrated into their ecosystems is intense, with Kaspi bank being a pioneer in this area since 2014. The bank is an example of a great success – it has 11.2 million monthly active users in the country with a population of 19.7 million.

Banking application as an access point to public services

The trend of banking applications being used as access points to public services simplifies the process for citizens and benefits the banks and governments. The report indicates that the banks are increasing transaction activity and cross-selling at the same time as the state is gaining access to the banks’ distribution channels and digital services.

The report cites Kaspi.kz (Kaspi bank) and Homebank (HalykBank) banking applications as examples. Both offer access to several public services, such as tax payment, individual entrepreneur registration and car sales and registration, which greatly streamlines the process of receiving public services and saves people’s time.

A growing number of SMEs are also adopting digital payments, prompting financial institutions to improve their credit scoring models using non-traditional data. It allows the banks to make more informed decisions, and reduces the risk of delayed loan payments. SMBs also get online services via banking applications for B2B transactions such as invoicing, accounting, fees and HR and legal support.

The democratization of the capital markets

The democratization of the capital markets has become one of the main trends in the financial sector in recent years. According to the report, legislative changes adopted in 2020 have increased retail investors in the country.

“Second-tier banks are now authorized to offer brokerage services to individuals. In addition, investment mobile apps have played a central role in democratizing access to the stock market, making it more accessible to retail investors. Biometric identification services are now available for external business relationships, and the need for traditional signature and identity card requirements has been removed,” the report states.

The report emphasizes the Kazakh government’s policy to develop a digital economy and innovations to accelerate the technological modernization of the economy over the past decade. The report shows that the country is firmly committed to developing the fintech industry by creating the necessary infrastructure and implementing digital reforms.

Tthe growth of start-ups and investment opportunities

Another trend identified by the report is the increase in the number of startups. The report noted that instead of disrupting the financial sector, the startups are now shifting towards B2B partnerships, driving change and growth in the industry.

According to MOST Ventures Managing Partner Pavel Koktyshev, the success of established companies such as Kaspi and new startups such as OneVision has led to an increase in investment in the fintech industry.

“OneVision, a fintech company offering a wide range of online payment services, was established in 2021 and has since expanded its operations to Kazakhstan, Azerbaijan, Uzbekistan and Kyrgyzstan. The success of these businesses shows how homegrown startups have the potential to make a big market impact and create a healthy ecosystem. As more entrepreneurs create new solutions, they strengthen the entire financial system and reduce the financial inclusion gap. Accordingly, Kazakhstan is well positioned to emerge as a regional hub for innovation and venture capital, Koktyshev said.

Regarding the regulatory framework for investors, the report noted that Kazakhstan has a classic fintech stakeholder setup. However, it is unique in Central Asia because there are two different jurisdictions with two regulators.

Astana International Financial Center (AIFC), one of the fintech stakeholders with a different jurisdiction operating under English law, has a holistic approach to developing the fintech ecosystem. The AIFC provides a number of benefits, including tax incentives on capital gains and dividends, a simplified registration process in English and electronic applications.

“Kazakhstan’s fintech market stands out as the largest in Central Asia, with remarkable growth rates placing it among the fastest growing fintech markets in Asia. This booming industry owes its success to the government’s explicit support, particularly through the AIFC, says Fintech Consult Managing Partner Dr. Jochen Biedermann.